The state of robotics

-

-

felix 这家伙很懒,还没有设置简介

1 人点赞了该文章 · 934 浏览

Our research shows companies are adopting robots, but it’s a long way to go before they’re commonplace.

By Bob Trebilcock· May 10, 2022

I will never forget ProMat 2007. That’s the first industry event where I saw what we now call autonomous mobile robots (AMR); more importantly, these were robots targeting warehousing and distribution. The exhibitors were Kiva Systems, now part of Amazon; RMT Robotics, now part of Cimcorp; and Seegrid. Each had relatively small booths where their vehicles moved around the space on their own like over-sized toys. While ProMat 2005 was all about RFID, AMRs were the hit of the 2007 show. Here’s what I wrote at the time:

“In 2007, RMT Robotics, Kiva Systems and Seegrid introduced mobile robots to the industry. They were to AGVs what go-karts are to Formula 1 race cars: small vehicles designed to move small loads. But what really distinguished them is that they had unique guidance systems that didn’t require fixed paths, such as magnetic tape on the floor or reflectors and lasers, to find their way around the facility. Instead, they could learn to find their way to almost any spot in a facility. Like ATLs (autonomous truck loading vehicles), they were the buzz of the show, even if no one quite knew what to do with them.”

Well, someone knew what to do with them. In 2010, RMT was acquired by Cimcorp. Then, in 2012, Amazon broke the bank, paying nearly $800 million for Kiva Systems, what I described at the time as “dot.com money.”

What best describes your organization’s use of robotic automation systems and/or autonomous mobile robots in your warehouses, distribution centers and/or manufacturing operations?

Source: Peerless Research Group (PRG)

At that time, goods-to-person picking was still a niche segment of the market. The real argument for robotics, I wrote then, wasn’t getting rid of labor, but dealing with a tight labor market. “Warehouses are struggling to keep enough workers to do the job, especially during seasonal and holiday spikes in demand… This is still very much an emerging trend, but it’s a trend that works in [robotics’] favor.”

Joe Buglewicz/Getty Images for Peerless Media

Fast forward a decade and 2012’s emerging tight labor market is an everyday fact of life for warehouse and distribution center managers. Only now, unlike in 2012, it’s coupled with rapidly rising wages. All of which might explain why you couldn’t walk down an aisle at Modex 2022 without tripping over a robot.

Instead of three small booths, dozens of robotics solution providers exhibited from around the globe. What’s more, every systems integrator worth their salt, regardless of size, had at least one robot on display. In some respects, it was a robotics show.

The other notable trend was the evolution from the point solutions on display at ProMat in 2007 to integrated solutions featuring multiple types of robots, such as a RightHand robot picking items to a Tompkins Robotics T-sort or a Hai Robotics’ case handling robot working in conjunction with a goods-to-person piece-picking station. It’s a whole new way of thinking about robotics in the DC.

Has the market finally figured out what to do with robots? In other words, are end users adopting or planning to adopt, or are they still just trying to understand the technology through small pilots, and taking a wait-and-see attitude toward rolling out projects?

Christopher Lane/Getty Images for Peerless Media

Those were among the questions Modern Materials Handling set out to answer in a survey launched right before Modex. The survey was developed in collaboration with The Robotics Group at MHI and WERC. It was distributed across our respective audiences (see box page 24).

For the purposes of this survey, we divided respondents into three categories: Those with no plans to use robots in the foreseeable future; those end users who are investigating the technology and plan to use it in the next two years; and those early adopters who already have robots up and running in their facilities.

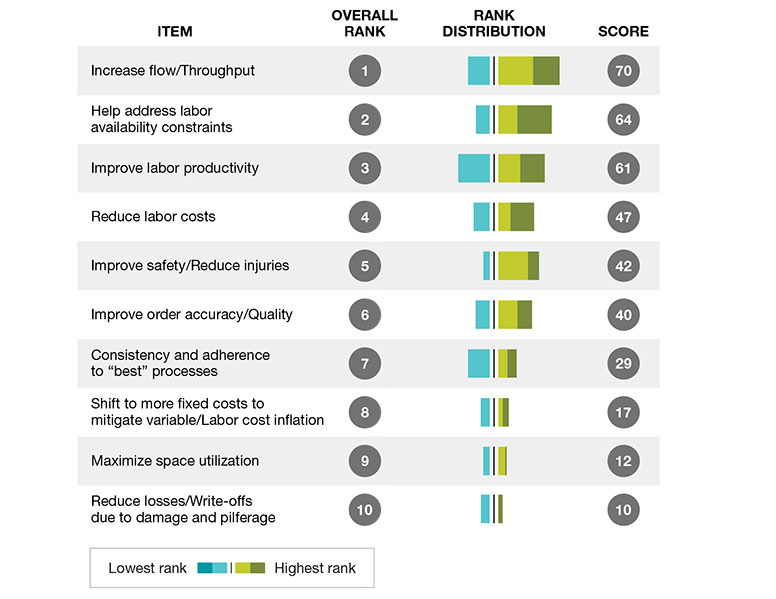

What are the Top 3 factors motivating your organization to pursue robotics in your warehouses and distribution centers?

Source: Peerless Research Group (PRG)

At a high level, we note three important takeaways:

- Adoption: Based on the survey results, the market is still split on the value from robotics.

- Labor: Those using robots, or interested in using robots, aren’t looking to replace labor. They are instead looking to make the most of their existing labor by augmenting processes.

- Value: A significant percentage of end users who have made the leap to adopt robotics are realizing their business case objectives, meeting their ROI goals and looking for ways to expand the use of robots into other areas of their operations.

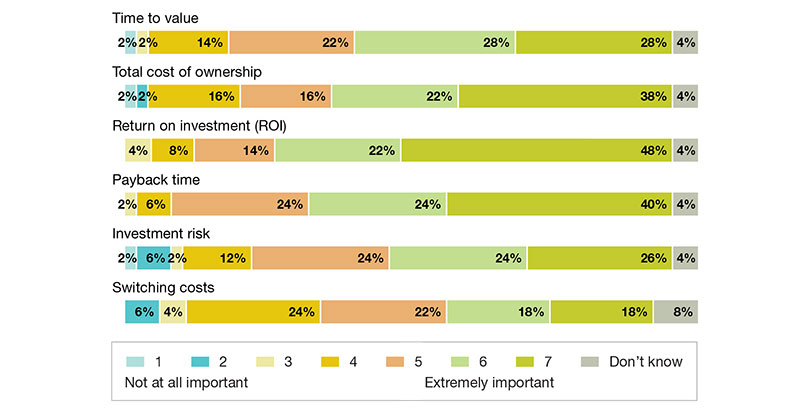

How important are the following business case factors when you are choosing your robotics solutions?

Source: Peerless Research Group (PRG)

No plans for robots

The question on everyone’s mind is: Robotics look great, but are people really using them (or planning to use them)?

The answer is a split decision: A slight majority (52%) is currently using robots in their plants and/or warehouses (23%); plans to adopt robotics within the next three years (21%); or has them on the technology roadmap for three or more years out (8%).

At the same time, nearly 48% of respondents said they have no plans to use robots at this time or don’t know about their future plans.

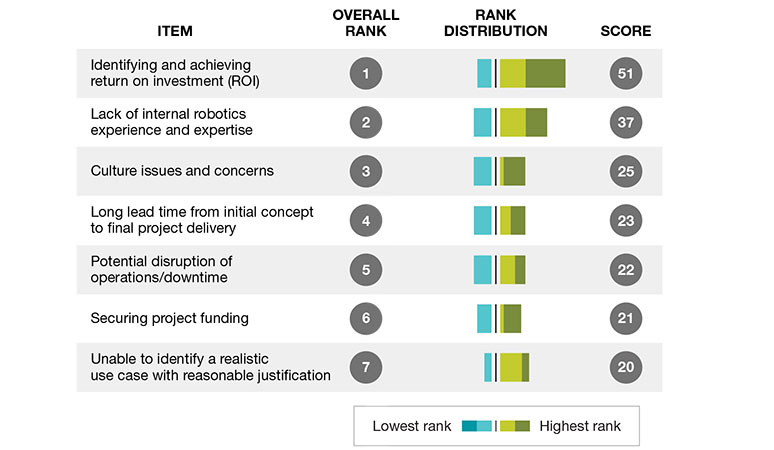

Among the top challenges to adoption identified by those respondents were:

- identifying and achieving an ROI;

- a lack of internal robotics expertise and experience;

- culture issues and concerns;

- long lead times from concept to final project delivery;

- the potential of disruption to operations or downtime from an implementation;

- securing funding for a robotics project; and

- the inability to identify a realistic use case with a reasonable justification.

What have been the Top 3 challenges or obstacles you have faced as you pursued robotics?

Source: Peerless Research Group (PRG)

Which use cases are you addressing with robots today?

Source: Peerless Research Group (PRG)

Other concerns included the maturity of robotics technology, the inability to find a partner to assist with a project and, finally, too many alternative options to sort through. Order fulfillment professionals might feel a little like the diner at the buffet; faced with so many options and sales pitches, they’re unsure of where to start to learn about the market.

Another hurdle appears to be a perception that robotics, like other forms of automation, are not suited to operations that involve customization versus more standard products and predictable orders.

“All of our orders are special orders, so we have no way to use robotic automation,” wrote one respondent. Another added “we would have to completely revamp our warehouse/shipping department, and many of our parts are oversize and not easily moved by robot, or the size of the robot we’d need to move them would be cost prohibitive.” And a third wrote: “All of our orders are different and generated by our customers. I don’t see how automation or robotic systems could be implemented in our business.”

Making the case for robotics

Companies planning to use robots in the near future have already gotten over some of those hurdles.

Asked to identify the most important business factors they considered in their decision to pursue robotics, 70% said that achieving an ROI was very or extremely important, while 64% identified the payback time as very or extremely important. Those were followed by total cost of ownership (60%), time to value (56%), investment risk (50%) and the cost of switching solutions (36%).

In most instances, funding was not an issue: Of the respondents planning to adopt robots, only 26% said they had not launched the funding process, while 32% said the funding process was underway, 24% said they had funding in place and the remainder said they could reallocate other funds or that pre-funding wasn’t needed because they planned to use a Robotics-as-a-Service (RaaS) model.

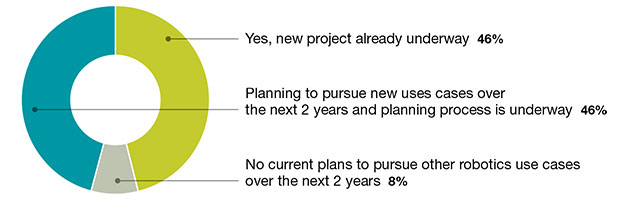

Do you plan to pursue other robotic automation use cases over the next 2 years?

Source: Peerless Research Group (PRG)

As to their robotics journey, 72% were in early stages, with 38% learning about the market and technology, 22% formulating their strategy and vision for robotics, 8% performing an impact analysis and 4% documenting their requirements.

Others were further along, with 12% planning to roll out additional robots based on previous successful tests, 2% about to implement their first robots in a live production environment and 2% piloting robots. The remainder either didn’t know or said they were doing something different.

Given the huge number of robotic solution providers and robot types, we wondered where the market is turning for information and help. As an example, end users typically turn to OEMs, consultants, system integrators and analyst firms like Gartner in traditional automation projects.

About our research

The “2022 Intralogistics Robotics Survey” was developed with input from The Robotics Group at MHI, WERC and editors at Peerless Media. The survey was distributed to the readers of Modern Materials Handling, Logistics Management and Supply Chain Management Review as well as members of MHI and WERC.

Survey results were drawn from 180 respondents with involvement with robotic automation systems or services. Nearly 34% were potential buyers or current users of robotics automation systems and/or robotics services.

Seven percent were suppliers of robotics systems and services, and 15% were consultants and systems integrators. They remainder indicated that they were not involved in robotic automation systems or services.

Respondents represented more than a dozen industries, with 42% in manufacturing, 18% in wholesale and retail trade, and 19% representing third-party logistics and transportation/warehousing service providers. The remaining 21% of respondents identified as “other non-manufacturing.”

Nearly 46% of respondents were from firms with less than $100 million in annual revenue, 18% from firms with less than $500 million in revenue and 22% with revenue between $500 million and more than $2.5 billion. Nearly 15% of respondents did not disclose their annual revenue.

Finally, 29% of respondents were senior leaders, including CEOs, presidents, GMs and VP level executives. Another 30% were operations leaders in plants, warehouses and distribution centers or logistics managers. Eight percent of respondents worked in procurement while 7% identified as industrial engineers.

Yet, many of the early adopters worked directly with robotic solution providers, in part because the solutions were point solutions. Where then are end users planning to use robots turning for information?

That, too, appears to be a mixed bag. The No. 1 source of information for this group was materials handling OEMs followed closely by robotic vendors. Next on the list were industry peers; systems integrators, industry analysts and advisory firms; and industry trade associations. Interestingly, the No. 5 answer was “we didn’t seek or need help.”

Asked to identify the top three factors motivating their pursuit robotics, respondents identified the need t

- increase flow/throughput,

- help address labor availability constraints,

- improve labor productivity,

- reduce labor costs,

- improve safety/reduce injuries,

- improve order accuracy/quality,

- consistency and adherence to best practices,

- shift to more fixed costs to mitigate variable/labor cost inflation,

- maximize space utilization, and

- reduce losses/write-offs due to damage and pilferage.

Similarly, respondents were asked which of the top three use cases were they considering for robotics. They were:

- picking,

- receiving and unloading,

- sorting,

- unit load/heavy payload transport,

- putaway into storage,

- order consolidation,

- packing,

- replenishment, and

- case/tote transport.

We also asked respondents to identify the types of robotics solutions they were considering. Respondents had the option of choosing more than one type:

- autonomous mobile robots (AMR) for pallet movement, 43.4%;

- AMRs for robot-to-goods picking or delivery to putwalls, 34%;

- piece-picking robots, 30%;

- pick-and-place robots for unit sorter induction, 30%;

- pallet handling AMRs, including forks and tuggers, 28%;

- sortation robots, 24%;

- stationary industrial robots, 22.6%;

- heavy payload carry-on-top transport robots for pallets, 19%;

- case/tote handling AMRs, 19%; and

- robotic putwalls, 15%.

Other processes included collaborative in-aisle picking, cleaning robots and mobile goods-to-person systems.

Asked their preferred commercial models for acquiring their robots, 46% indicated they planned to purchase an entire solution, including the hardware, software, maintenance and support.

An equal percentage planned to subscribe to a RaaS model (24%), in which the solution provider is responsible for all of the above or buy the robot but subscribe to a Software-as-a-Service (SaaS) model (22%) for software and support.

Robots in action

End users who have already implemented robotics in their operations were the last category of respondents. They represented a continuum of stages in their development.

For instance, 28% reported that they have fully deployed robotics across one or more locations, and another 17% have more than three different deployments underway. Eleven percent said they have fully deployed one type of robot and are in the process of deploying one other type of robot. Clearly, in the population or respondents using robots, there is a lot of activity.

Meanwhile, 17% of respondents are piloting robotics, 6% are implementing their first live production environment and 6% are now deploying across multiple locations.

What are the primary types of robotic automation systems you will likely consider in the next 2 to 5 years?

Source: Peerless Research Group (PRG)

Asked if they would expand the size of their existing robotic automation systems over the next two years, an equal percentage of respondents (39%) indicated they would make small increases to the sizes of their fleets and significant increases in the size of the fleet across multiple facilities. Another 8% indicated plans for a significant increase in the fleet in a single facility. Fifteen percent said they did not currently know their plans.

Their reasons for implementing robots mirror those of the organizations currently investigating the market with plans to implement in the future: Address labor constraints, increase flow and throughput, improve labor productivity, reduce labor costs and maximize space utilization topped the list.

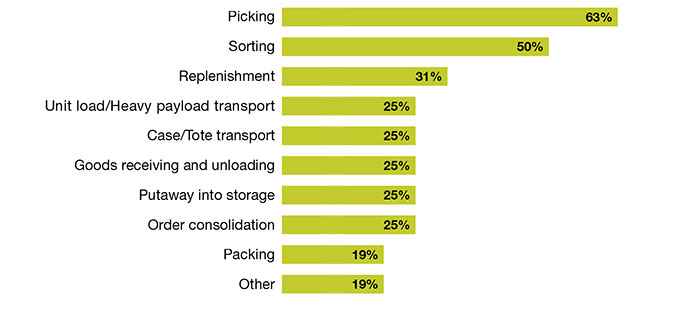

As to the use cases being addressed today with robots, picking topped the list:

- picking, 63%;

- sorting, 50%;

- replenishment, 31%;

- unit load/heavy payload transport, 25%;

- case/tote transport, 25%;

- receiving and unloading, 25%;

- putaway into storage, 25%;

- order consolidation, 25%; and

- packing, 19%.

The types of robots already in use by the early adopters reflect the priorities around use cases, with robotic picking systems accounting for 50% of the robots in use. They were followed by

- case/tote handling AMRs, 43%;

- sortation robots, 36%;

- mobile goods-to-person systems, 29%;

- AMRs for robot-to-goods picking or delivery to putwalls, 29%;

- stationary industrial robots, 21%;

- heavy payload carry-on-top transport robots for pallets, 14%;

- pallet handling AMRs, including forks and tuggers, 14%; and

- collaborative in-aisle picking, 7%.

Finally, reflecting processes using multiple robots on display at Modex, we asked end users if they planned to pursue other robotic automation use cases over the next two years.

Eight percent said they had no current plans to pursue other use cases. Meanwhile, 46% not only plan to pursue new use cases over the next two years, they have already launched the planning process. Another 46% responded that new projects are already underway.

As to the primary types of robotics they’re likely to consider in the next two to five years, mobile goods-to-person systems topped the list (62%), followed by robotic picking systems (54%), sortation robots (46%), robotic putwalls (39%) and heavy payload carry-on-top transport robots for pallets and unit loads (31%).

Just as early adopters of voice technology began with picking and then looked for other use cases to leverage the technology, early adopters of robotics are looking for ways to get more from the technology.

Where’s the ROI?

While the robotics industry has promoted a subscription-based RaaS model, popular with third-party logistics providers (3PL), 62% of respondents indicated that they purchased the entire robotics solution, including providing their own maintenance and support as a pure capital expenditure play. Just under a third (31%) opted for an RaaS model, and another 8% bought the robots but subscribe to a SaaS model for software and support.

At the end of the day, the question mark around robotics technology is whether it’s the shiny new object or delivering real value. To that end, 85% of respondents said their investments met (54%) or exceeded (31%) their ROI objectives. Another 77% said they met (54%) or exceeded (23%) the payback time and a similar percentage said they met or exceeded their time to value objectives.

Only 15% of respondents reported that the payback time failed to meet their objectives. The one significant outlier was total cost of ownership. Here, 54% said their investment met (31%) or exceeded (23%) their objectives, while 31% said they failed to meet their objectives.

As to their overall business goals, 69% of respondents said their investment in robotics met their goal, while 23% said it had not.

When it comes to the top three challenges that influenced their investments in robotics, end users cited the potential disruption of operations as No. 1, followed by building a realistic business case and justifying the investment, identifying and achieving an ROI, securing project funding, the risk of the project and knowledge about the market and the other materials handling automation options.

If you walked the floor at Modex, it’s clear the solution provider community sees a bright future in robotics. It’s also clear from our survey results that the market is still straddling the fence: About half of the survey respondents are unconvinced that robotics can deliver value to their organizations; the other half has either already stuck its toes in the water or is preparing to do so.

What comes across strongly is that a significant percentage of early adopters are meeting their business objectives, have realized an ROI and time to value, and are looking to expand their use of robotics and leverage their investments.

全部 0条评论